Basic Taxation Law: Estate Tax

Estate Tax

Preliminary

Article 712 of the New Civil Code provides for the different modes of acquiring ownership, namely: OIL-DSTP

occupation

intellectual creation

Law

succession, whether testate or intestate

tradition, as consequence of certain contracts,

prescription.

Of these modes of acquiring ownership, succession and donation are generally regarded as gratuitous transfers of property from one person to another which means there is no consideration involved in the transfer or acquisition of property.

These transfers are, however, subject to corresponding transfer taxes.

Transfer tax

The tax on the gratuitous transfer of property is called transfer tax.

Under the National Internal Revenue Code (NIRC or Tax Code), as amended, there are two (2) transfer taxes namely:

Estate tax under Section 84 and

Donor's tax under Section 98.

In addition, there is another transfer tax under Section 135 of the Local Government Code, which is the Tax on Transfer of Real Property Ownership imposed by the province and city.

However, this transfer lax is not solely imposed on gratuitous transfer of property but also on sale, barter, or any other mode of transferring ownership or title of real property, which generally involve a consideration.

Moreover, it is apparent that the transfer tax in Section 135 of the Local Government Code applies only to real property, while estate and donor's tax apply to both personal and real properties.

Estate tax

Estate tax is a tax on the exercise of the right to transfer property at death and is measured by the value of the property.

Pablo Lorenzo v. Juan Posadas, Jr., G.R. No. L 43082,June 18, 1937:

It accrues as of the date of death of the decedent, notwithstanding the postponement of the actual possession or enjoyment of the estate by the beneficiary.

By nature, estate tax is not a property tax but the value of the property serves as the basis of the tax.

Estate tax is an excise tax or a privilege tax.

Estate tax is in the nature of administration expenses payable out of any available funds of the estate; and if there be none, by converting any property into money for such purpose.

Theories of Estate Taxation

The imposition of estate tax is based on the following theories: BRAS

Benefit-Received Theory

The government performed services in the distribution of the properties of the decedent to the heirs.

In view of these services and benefits derived both by the estate and the heirs, the state collects the tax.

Redistribution of Wealth Theory

The imposition of estate tax reduces the property received by the successor bringing about a more equitable distribution of wealth in society.

The portion of the property taken by the state in the form of tax is then used to fund social programs and projects of the state.

Ability-to-Pay Theory

The bigger the estate means the higher taxes to be paid.

If the decedent dies without any property or if the properties are sufficient to cover some of the deductions allowed, then there is no liability to pay the tax; and

State Partnership Theory

The state is viewed as a passive and silent partner in the accumulation of wealth and property of the decedent.

The state even grants protection to the large estate of the decedent.

The state collects its just share in such an effort at the right time.

Governing Law on Imposition of Estate Tax

Well-settled is the rule that estate taxation is governed by the statute in force at the time of death of the decedent.

Pablo Lorenzo v. Juan Posadas, G.R. No. L-43082, June 18, 1937; Section 3, Revenue Regulations No. 2-2003:

The estate tax accrues as of the date of death of the decedent and the accrual of the tax is distinct from the obligation to pay the same.

Upon the death of the decedent, succession takes place and the right of the State to tax the privilege to transmit the estate vests instantly upon death.

For purposes of estate tax, the following are the relevant tax laws and their respective dates of effectivity:

Revised Administrative Code

March 1, 1917 - October 28, 1936

Commonwealth Act No. 106

October 29, 1936 - June 30, 1939

Commonwealth Act No. 466

July 1, 1939 - September 14, 1950

Republic Act No. 579

September 15, 1950 - December 31, 1972

Presidential Decree No. 69

January 1, 1973 - December 31, 1985

Presidential Decree No. 1994

January 1, 1986 - July 27, 1992

Republic Act No. 7499

July 28, 1992 - December 31, 1997

Republic Act No. 8424 (NIRC of 1997)

January 1, 1998 - December 31, 2017

Republic Act No. 10963 (Tax Reform for Acceleration and Inclusion (TRAIN) Law)

January 1, 2018 up to present

In fine, even if the estate of the decedent is being settled at present time, one must look at the date of death of the decedent to determine the applicable law in the settlement of estate and the computation of estate tax liability.

Again, it is not the law effective at the time the estate is settled, but the law enforced at the date or time of death of the decedent that will govern the settlement of his estate.

Taxpayer of Estate Tax and Liability for Payment

The "estate" is the statutory taxpayer of estate tax.

The "estate" is treated as a person for purposes of paying the taxes.

In fact, there is a separate taxpayer identification number (TIN) that the BIR issues to the estate for the purpose of filing the estate tax return and the payment of estate tax.

The estate tax imposed is, however, paid by the executor or administrator before the delivery of the distributive share in the inheritance to any heir or beneficiary.

Where there are two or more executors or administrators, all of them are severally liable for the payment of the tax.

The estate tax clearance issued by the Commissioner of Internal Revenue (CIR or Commissioner) or the Revenue District Officer (RDO) having jurisdiction over the estate, serves as the authority to distribute the remaining distributable properties/share in the inheritance to the heir or beneficiary.

The executor or administrator of an estate has the primary obligation to pay the estate tax, but the heir or beneficiary has subsidiary liability for the payment of that portion of the estate which his distributive share bears to the value of the total net estate.

The extent of his liability, however, shall in no case exceed the value of his share in the inheritance.

Determination of Estate Tax Liability

The estate tax is determined by multiplying the appropriate estate tax rate with the net taxable estate, its tax base.

In general, the estate tax is computed as follows:

Net Taxable Estate = Gross Estate − Deductions

Estate Tax Due = Net Taxable Estate x Estate Tax Rate

Estate Tax Still Due = Estate Tax Due − Tax Credits

The above formula may vary depending on whether the decedent is single or married at the time of death.

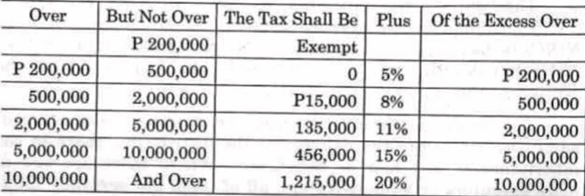

Estate Tax Rate

NIRC:

Under the NIRC, the estate tax is computed using the following schedular and progressive tax rates:

Based on the table of rates above, a net taxable estate of P200,000.00 or less is exempt from estate tax.

TRAIN Law

The estate tax rate is modified upon the enactment of TRAIN Law.

Effective January 1, 2018, estate tax is computed at six percent (6%) of the net taxable estate.

This means a flat rate of six percent (6%) applies regardless of the amount of net taxable estate.

This also means that the first P200,000.00 net taxable estate is no longer exempt.

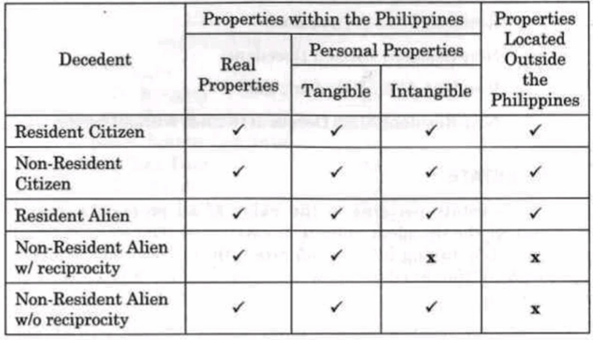

Classification of Decedent

The classification of a decedent is important because it determines the properties included in the gross estate, the deductions that may be claimed, and the place of filing of the return.

A decedent may be classified based on citizenship and last residence at the time of death.

A decedent may either be:

Resident Citizen Decedent;

Non-Resident Citizen Decedent;

Resident Alien Decedent; and

Non-Resident Alien Decedent (with or without reciprocity)

Gross Estate

Gross estate pertains to the value of all properties, real or personal, of the decedent subject to estate tax.

The gross estate is determined by taking into consideration the citizenship, residence, and status of the decedent, as well as the location of the properties of the decedent.

The gross estate of a decedent who is a resident citizen, non resident citizen, and resident alien comprises of all properties, real or personal, tangible or intangible, wherever situated, and interest therein at the time of his death, including transfer in contemplation of death, revocable transfers, property passing under the general power of appointment, and transfers for insufficient consideration.

On the other hand, the gross estate of a decedent who is a non-resident alien comprises only of properties situated in the Philippines. With respect to intangible personal property located in the Philippines, its inclusion in the gross estate is subject to the rule of reciprocity provided for under Section 104 of the Tax Code.

In summary, the gross estate is comprised of the following:

Gross Estate = Properties Owned and Existing at the Time of Death of the Decedent − Exempt Transmissions/Acquisitions (Excluded Properties) + Taxable Transfers (Other inclusions)

Inclusions to Gross Estate

General Rule: All properties owned by the decedent and existing at the time of his death are included in the gross estate.

These inclusions in the gross estate may be summarized as follows:

Reciprocity Rule

As presented in the table above, a non-resident alien decedent is taxable only on properties, real and personal, situated in the Philippines.

Personal properties may either be tangible or intangible.

The inclusion of intangible personal properties in the gross estate of the non-resident alien decedent depends on whether the reciprocity rule applies or not.

The reciprocity rule applies only to a non-resident alien decedent and only on his intangible personal properties located in the Philippines.

The reciprocity rule provides that no estate tax will be collected in respect of intangible personal property in the following instances:

if the decedent at the time of his death was a citizen and resident of foreign country which at the time of his death did not impose estate tax, in respect of intangible personal property of citizens of the Philippines not residing in that foreign country, or

if the laws of the foreign country of which the decedent was a citizen and resident at the time of his death allows a similar exemption from transfer or death taxes of every character or description in respect of intangible personal property owned by citizens of the Philippines not residing in that foreign country.

The reciprocity rule is by nature a form of exemption from estate tax because if the non-resident alien can avail this rule, the intangible personal properties located in the Philippines are not included in the gross estate and therefore not subject to estate tax.

Section 104 of the Tax Code provides the intangible personal a. b properties deemed located in the Philippines, to wit: F-C85A-P

Franchise exercised in the Philippines;

Shares, obligations, or bonds issued by any corporation or sociedad anonima organized or constituted in the Philippines in accordance with its laws;

Shares, obligations or bonds by any foreign corporation eighty-five percent (85%) of the business of which is located in the Philippines;

Shares, obligations or bonds issued by any foreign corporation if such shares, obligations, or bonds have acquired a business situs in the Philippines; and

Shares or rights in any partnership, business, or industry established in the Philippines.

To emphasize, before the reciprocity rule may apply, a decedent must be a citizen and resident of a foreign country that does not impose estate tax or grants exemption thereto.

If a decedent is a citizen of one foreign country but a resident of another foreign country at the time of his death, e.g, a Singaporean residing in Japan at the time of death, the reciprocity rule cannot be applied.

Collector of Internal Revenue v. Antonio Campus Rueda, G.R. No. L-13250, October 29, 1971:

The decedent was a Spanish national but a resident of Tangier, Morocco. At the time of her death, she owned intangible personal properties located in the Philippines.

The laws of Morocco allow exemption from transfer taxes with respect to intangible personal properties by citizens of the Philippines in Morocco.

The Supreme Court in this case allowed the application of the reciprocity rule and granted exemption from estate tax on the intangible personal properties located in the Philippines.

It must be emphasized that the Collector of Internal Revenue v. Antonio Campus Rueda arose and was decided under National Internal Revenue Code of 1939 where then Section 122 (now Section 104) only requires that the decedent at the time of his death was a resident of a foreign country which does not impose estate tax or grants exemption thereto.

As it is now under Section 104 of the Tax Code, the requirement is that the decedent must be a citizen and resident of a foreign country for the reciprocity rule to apply.

Another issue resolved in Collector of Internal Revenue v. Antonio Campus Rueda is the argument of the BIR that the reciprocity rule cannot be applied because Morocco, at that time, was not a country, hence the exemption cannot be applied.

The Supreme Court ruled that being a country for purposes of the applicability of rule on reciprocity is immaterial.

If the laws of Morocco grant exemption from transfer taxes with respect to intangible personal properties owned by citizens of the Philippines in Morocco, the requirement to be exempt is satisfied.

Exclusions to Gross Estate

The gross estate of the decedent does not include: ET/EP

exempt transmissions/acquisitions and

excluded properties even if they are existing and with the decedent at the time of death.

Exempt Properties

The following acquisitions and transmissions are exempt from estate tax, and thus, shall not be taxed: UF-FS

The merger of usufruct in the owner of the naked title;

The transmission or delivery of the inheritance or legacy by the fiduciary heir or legatee to the fideicommissary;

The transmission from the first heir, legatee, or donee in favor of another beneficiary, in accordance with the desire of the predecessor; and A

ll bequests, devises, legacies, or transfers to social welfare, cultural and charitable institutions.

As conditions for exemption of transfers to social welfare, cultural, and charitable institutions, no part of the net income of social welfare, cultural, and charitable institutions must inure to the benefît of any individual, and not more than thirty percent (30%) of the said bequests, devises, legacies or transfers are used by such institutions for administration purposes.

Excluded Properties

The gross estate does not include the capital of the surviving spouse of a decedent.

In addition, the net share of the surviving spouse in the conjugal partnership property as diminished by the obligations properly chargeable to such property is also not included in the estate of the decedent.

Taxable Transfers

Taxable transfers are transfers of properties during the lifetime of the decedent or transfers inter-vivos.

Considering that the transfer happened during the lifetime of the decedent, the properties involved are no longer with the decedent at the time of his death and supposedly not included in his gross estate anymore.

However, the nature and circumstances attending the transfers indicate that the transfers are actually transfers mortis causa or suggest that the decedent still owns and controls properties up to the date of his death.

Hence, these transfers of properties must be included in the gross estate and are subject to estate tax.

The taxable transfers are: TRPT

Transfer in contemplation of death;

Revocable transfer;

Property passing under general power of appointment; and

Transfers for insufficient consideration.

a. Transfer in Contemplation of Death Section 85(B)

A transfer made in contemplation of death is one prompted by the thought that the transferor has not long to live and made in place of a testamentary disposition.

Contemplation of death is a state of mind and it cannot be easily ascertained, unless he says so, that the person is transferring the property because he knows he would die anytime soon.

In this case, the acts and circumstances present before, during, or after the transfer are considered to ascertain whether the transfer is in contemplation of death.

The health condition and age of the decedent, the execution of last will and testament, and the time gap between the transfer and the death of the transferor are factors suggesting the transfer is in contemplation of death.

b. Revocable Transfer Section 85(C)

Revocable transfer is a transfer of property where such property continues to be owned by the transferor-trustor during his lifetime notwithstanding the transfer, as he still retains beneficial ownership.

Simply, revocable transfer involves transfer of possession over the property during the lifetime of the decedent but not transfer of ownership over the said property.

Section 85(C) of the Tax Code, as amended, provides that interest in the property of which the decedent has at any time made a transfer by trust or otherwise is included in the decedent's gross estate.

The value of the gross estate of the decedent shall be determined by including the value at the time of his death of all properties, real or personal, tangible or intangible, wherever situated to the extent of any interest therein, of which the decedent has at any time made a transfer by trust, where the enjoyment thereof was subject at the date of his death to any change through the exercise of a power by the decedent to alter, amend, revoke, or terminate, or where any such power is relinquished in contemplation of the decedent's death.

The rationale for taxing such transfer in trust at the time of death of the trustor is to reach transfers which are really substitutes for testamentary dispositions and thus prevent evasion of estate tax.

To be exempt from estate tax, the transfer inter vivos must be absolute and outright with no strings attached whatsoever by the transferor, which is not the case here.

c. Property Passing under General Power of Appointment Section 85(D)

"Power of appointment" refers to a right to designate the person or persons who shall enjoy or possess certain property from the estate of a prior transferor.

There are two (2) parties involved in the property passing under the power of appointment namely, the donor of power and the donee of power.

The "donor of power" is a person having property subject to disposition who created, reserved, or granted the power to designate the transferees or recipients of the property.

The "donee of power" is a person to whom the power to designate the transferees or recipient of the property is given or conferred.

For estate tax purposes, the "donee of power" is the decedent.

"Power of appointment" may either be:

General Power of Appointment

It authorizes the donee the power to appoint any person he pleases, including himself, his spouse, his estate, executor or administrator, and his creditor, thus having as full dominion over the property as though he owned it, or

Special Power of Appointment

when the donee can appoint only among a restricted or designated class of persons other than himself.

A property passing under a general power of appointment is included in the gross estate of the donee-decedent while a property passing under a special power of appointment is not included in the gross estate of the donee-decedent.

Thus, under Section 85D of the NIRC, the property is included in the gross estate if the following are present:

The property passed under a general power of appointment;

The exercise of the decedent of such power is:

by will, or

by deed executed in contemplation of, or intended to take effect in possession or enjoyment at or after his death, or

by deed under which he has retained for his life or any period not ascertainable without reference to his death or for any period which does not in fact end before his death:

the possession or enjoyment of, or the right to the income from, the property, or

the right, either alone or in conjunction with any person, to designate the persons who shall possess or enjoy the property or the income therefrom.

The above rule, however, does not apply in case of a bona fide sale for an adequate and full consideration in money or money's worth.

d. Transfers for Insufficient Consideration Section 85(G)

Inclusion in Gross Estate:

Under Section 85(G) of the TaxCode, if any one of the transfers, trusts, interests, rights, or powers enumerated and described in Subsections (B), (C), and (D) of Section 85 of Tax Code is made, created, exercised, or relinquished for a consideration in money or money's worth, but is not a bona fide sale for an adequate and full consideration in money or money's worth, there shall be included in the gross estate only the excess of the fair market value, at the time of death, of the property otherwise to be included on account of such transaction, over the value of the consideration received therefor by the decedent.

Gratuitous Transfers:

When the circumstances of the transfers of property are those described in Section 85(B), (C), and (D) of the Tax Code and the transfers are without consideration, the transfers are called as transfers in contemplation of death, revocable transfers, or property passing under a general power of appointment.

This means the transfers are gratuitous.

Insufficient Consideration:

However, when the circumstances of the transfer of property are those described in Section 85(B), (C), and (D) of the Tax Code and the transfer is for inadequate or less than full consideration in money or money's worth, the transfer is a transfer for insufficient consideration and is subject to estate tax.

Bona Fide Sales:

When the circumstances of the transfers of property are those described in Section 85(B), (C), and (D) of the Tax Code and the transfers are for adequate or full consideration in money or money's worth, the transfers are bona fide sales and therefore not subject to estate tax.

Donor's Tax:

It must be noted that when the circumstances of the transfer of property are not those described in Section 85(B), (C), and (D) of the Tax Code and the transfer is for inadequate or less than full consideration in money or money's worth, the transfer is a transfer for less than adequate and full consideration described in Section 100 of the Tax Code, which transfer is subject to donor's tax.

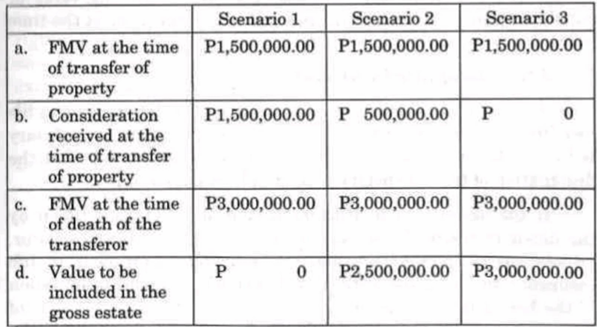

The transfer is for insufficient consideration if the fair market value of the property at the time of transfer is substantially higher than the consideration received at the time of said transfer.

In this case, the value included in the gross estate or the value subject of estate tax is the difference between the consideration received and the fair market value of the property at the time of death of the transferor.

Gross Estate = Fair Market Value at Time of Death − Consideration Received

Illustration

Scenario 1:

The fair market value at the time of transfer of property is equal to the consideration received at the time of transfer.

The transfer is a bona fide sale and therefore not subject to estate tax.

Scenario 2:

The fair market value at the time of transfer of property is higher than the consideration received at the time of transfer of property.

The transfer is for insufficient consideration.

The value to be included in the gross estate is the difference between the consideration received and the fair market value of the property at the time of death of the transferor.

Scenario 3:

This is a case of donation mortis causa because the transfer is without any consideration.

The full fair market value of the property at the time of death of the transferor is included in the gross estate.

Again, to be subject to estate tax, the transfer for insufficient consideration must be coupled with circumstances of the transfer of property in Section 85 (B), (C), and (D) of the Tax Code.

Other Inclusions

Other inclusions in the gross estate are decedent's interest, proceeds of life insurance, and prior interest.

a. Decedent's Interest

Decedents interest pertains to any interest having value or capable of being valued and transferred by the decedent at the time of his death.

b. Proceeds of Life Insurance

The proceeds of life insurance taken by the decedent upon his own life are included in the gross estate if the designated beneficiary is his estate, executor, or administrator, regardless of whether the designation of he beneficiary is revocable or irrevocable.

If the designated beneficiary in the life insurance taken by the decedent upon his own life is other than his estate, executor, or administrator, the inclusion or exclusion of proceeds of life insurance in the gross estate is determined by the designation of the beneficiary.

If the designation is revocable, the proceeds of life insurance are included in the gross estate.

Otherwise, if the designation is irrevocable, the proceeds of life insurance are excluded from the gross estate.

Thus, the proceeds of the following insurance are not included in the gross estate of the decedent, and not subject to estate tax: AGGA

Policy is an accident or property insurance;

Policy is taken by the employer for his employees or the so-called group life insurance;

Proceeds of insurance issued by the Government Service Insurance System (GSIS) and Social Security System (SSS) for government and private employees, respectively; and

Proceeds of life insurance payable to the heirs of the deceased members of the US and Philippine Army.

Life insurance is a tax-efficient method of transfer of property, specifically money, from one person to another.

If a person took a life insurance upon his own life, the proceeds are exempt from estate tax as discussed above.

Similarly, the heirs who received the proceeds of life insurance are not subject to income tax because the proceeds of life insurance received by the heirs or beneficiaries are excluded from the gross income and therefore not subject to income tax under Section 32 (B)(1) of the Tax Code.

c. Prior Interest

Except as otherwise specifically provided therein, transfer in contemplation of death, revocable transfer, and proceeds of life insurance shall apply to the transfers, trusts, estates, interests, rights, powers, and relinquishment of powers, as severally enumerated and described therein, whether made, created, arising, existing, exercised, or relinquished before or after the effectivity of the Tax Code.

Determination of Value of the Gross Estate

As estate tax accrues at the time of death, the properties comprising the gross estate are valued based on their fair market value as of the time of death.

Usufruct

to determine the value of the right to usufruct, use or habitation, as well as that of annuity, there shall be taken into account the probable life of the beneficiary in accordance with the latest basic standard mortality table, to be approved by the Secretary of Finance, upon recommendation of the Insurance Commissioner.

Real Property

the fair market value is whichever between:

The fair market value as determined by the Commissioner of Internal Revenue, usually called as the Zonal Value, and

The fair market value as shown in the schedule of values fixed by the provincial and city assessors.

For purposes of prescribing real property values, the Commissioner of Internal Revenue is authorized to divide the Philippines into different zones or areas and shall, upon consultation with competent appraisers both from the private and public sectors, determine the fair market value of real properties located in each zone or area.

Shares of Stocks

the valuation of the shares of stock will be:

If the share is listed in the stock exchange, the fair market value is the price quote on the date of death.

If there is no available price quote on the date of death, the fair market value is the arithmetic mean between the highest and lowest quotation at a date nearest the date of death.

If the share is unlisted in the stock exchange:

Unlisted common shares are valued based on their book value; and

Unlisted preferred shares are valued at par value.

In determining the book value of common shares, appraisal surplus is not considered as well as the value assigned to preferred shares, if there are any.

Deductions

In computing the net taxable estate, there are deductions allowed by law depending on who the decedent is.

These deductions under the Tax Code are classified into: OSS

Ordinary Deductions EPT

Expenses, Losses, Indebtedness, Taxes, etc. (ELITE): FJ-CC-UUL

Funeral Expense;

Judicial Expense;

Claims Against the Estate;

Claims Against Insolvent Person;

Unpaid Mortgage;

Unpaid Taxes; and

Losses.

Property Previously Taxed or Vanishing Deduction; and

Transfer for Public Use.

Special Deductions FMBS

Family Home;

Medical Expenses;

Benefits Received under Republic Act No. 4917; and

Standard Deduction.

Share of the Surviving Spouse

The classification of the decedent is important because the estates of a resident citizen, non-resident citizen, and resident alien decedent may claim both:

✅ ordinary and

✅ special deductions.

With respect to a non-resident alien decedent, his estate may only claim:

✅ ordinary deductions but

❌ not special deduction.

In addition, the non resident alien decedent can only claim pro-rated:

✅ expenses, losses, indebtedness, and taxes.

If the decedent is married, the share of the surviving spouse in the net conjugal properties is deducted from the gross estate of the decedent.

General Principles of Estate Deductions

In claiming the deduction, the following principles apply:

Substantiation Rule

All items of deductions must be supported with documentary evidence such as receipts, invoices, contracts, financial statements, and other proof that they actually existed or occurred to establish their validity.

The only exception to this rule is the Standard Deduction.

Matching Principle

An item of deduction must be part of the gross estate to be deductible therefrom.

No deduction is allowed for those which are not part of the gross estate.

No Double Classification Rule

An item of deduction cannot be claimed under several deduction classifications.

Only one classification is allowable.

Default Presumption on Ordinary Deduction

In the case of married decedents, ordinary deductions are presumed to be against the common properties unless proven to be exclusive property of either spouse.

This is in line with the rule that properties are common properties unless proven exclusive.

Deductions Allowed to Estate of Citizen and Resident Decedent

Funeral Expense

Funeral expenses are expenses incurred from the date of death until the date of interment.

Funeral expenses are not confined to its ordinary or usual meaning. They include:

✅ The mourning apparel of the surviving spouse and unmarried minor children of the deceased bought and used on the occasion of the burial;

✅ Expenses for the deceased's wake, including food and drinks;

✅ Publication charges for death notices;

✅ Telecommunication expenses incurred in informing relatives of the deceased;

✅ Cost of burial plot, tombstones, monument or mausoleum but not their upkeep.

In case the deceased owns a family estate or several burial lots, only the value corresponding to the plot where he is buried is deductible;

✅ Interment and/or cremation fees and charges; and

✅ All other expenses incurred for the performance of the rites and ceremonies incident to interment.

❌ Expenses incurred after the interment, such as for prayers, masses, entertainment, or the like are not deductible.

❌ Any portion of the funeral and burial expenses borne or defrayed by relatives and friends of the deceased are not deductible.

❌ Medical expenses as of the last illness will not form part of funeral expenses but should be claimed as a Medical Expense, a special deduction.

Actual funeral expenses shall mean those which are actually incurred in connection with the interment or burial of the deceased.

The expenses must be duly supported by receipts or invoices or other evidence to show that they were actually incurred following the substantiation rule.

The amount that may be claimed as funeral expense is whichever is lower between:

actual funeral expenses (whether paid or unpaid) up to the time of interment, or

five percent (5%) of the value of gross estate.

The claimable funeral expense shall in no case exceed P200,000.00.

❌ Any amount of funeral expenses in excess of the P200,000.00 threshold, whether the same had actually been paid or still payable, is not be allowed as a deduction.

❌ Neither is the unpaid portion of the funeral expenses incurred, which is in excess of the P200,000.00 threshold allowed to be claimed as a deduction under "claims against the estate" following the No Double Classification Rule.

TRAIN Law

TRAIN Law repealed the provision allowing funeral expense as an ordinary deduction.

Thus, estates of decedents who died on January 1, 2018 onwards may no longer claim funeral expense.

Judicial Expense

Judicial expenses are expenses for testamentary or intestate proceedings which include expenses incurred in the inventory taking of assets comprising the gross estate, their administration, the payment of debts of the estate, as well as the distribution of the estate among the heirs.

In short, these deductible items are expenses incurred during the settlement of the estate but not beyond the last day prescribed by law, or the extension thereof, for the filing of the estate tax return.

Judicial expenses may include:

✅ Fees of executor or administrator;

✅ Attorney's fees;

✅ Court fees;

✅ Accountant's fees;

✅ Appraiser's fees;

✅ Clerk hire;

✅ Costs of preserving and distributing the estate;

✅ Costs of storing or maintaining property of the estate; and

✅ Brokerage fees for selling property of the estate.

Any unpaid amount for the aforementioned cost and expenses claimed under "Judicial Expenses" should be supported by a sworn statement of account issued and signed by the creditor following the Substantiation Rule.

Judicial expenses are expenses of administration.

Administration expenses, as an allowable deduction from the gross estate of the decedent for purposes of arriving at the value of the net estate, have been construed to include all expenses essential to the collection of the assets, payment of debts or the distribution of the property to the persons entitled to it.

Commissioner of Internal Revenue v. Josefina Pajonar, G.R. No. 123206, March 22, 2000:

✅ Judicial expenses include expenses incurred in the judicial proceeding or extrajudicial settlement of the estate.

B. E. Johannes v. Carlos Imperial, G.R. No. L-19153, June 30, 1922:

❌ However, expenditures incurred for the individual benefit of the heirs, devisees, or legatees are not deductible.

❌ Judicial expense does not also include fees incident to litigation incurred by the heirs in asserting their respective rights.

TRAIN Law

TRAIN Law repealed the provision allowing judicial expense as an ordinary deduction.

Thus, estates of decedents who died on January 1, 2018 onwards may no longer claim judicial expense.

Claims Against the Estate

In claims against the estate, the decedent is the debtor.

The word "claims" is generally construed to mean debts or demands of a pecuniary nature which could have been enforced against the deceased in his lifetime and could have been reduced to simple money judgments.

Claims against the estate or indebtedness in respect of property may arise out of contract, tort, or operation of law.

Requisites for Deductibility of Claims Against the Estate

In order to avail claims against the estate as a deduction to determine the net taxable estate, the following essential requisites must be present: PGVN

The liability represents a personal obligation of the deceased existing at the time of his death except:

unpaid obligations incurred incident to his death such as unpaid funeral expenses (i.e., expenses incurred up to the time of interment) and)

unpaid medical expenses, which are classified under a different category of deductions;

The liability was contracted in good faith and for adequate and full consideration in money or money's worth;

The claim must be a debt or claim, which is valid in law and enforceable in court;

The indebtedness must not have been condoned by the creditor or the action to collect from the decedent must not have been prescribed.

It is also required of claims against the estate as allowable deduction that: DS

at the time the indebtedness was incurred, the debt instrument was duly notarized and,

if the loan was contracted within three (3) years before the death of the decedent, the administrator or executor is required to submit a statement showing the disposition of the proceeds of the loan.

Claims Against Insolvent Person

In claims against an insolvent person, the decedent is the creditor.

The claim is incurred during the lifetime of the decedent but remains unpaid at the time of his death.

Thus, it is the estate which is now collecting from the debtors of the decedent.

The debtor must be insolvent.

Insolvent refers to the financial condition of a debtor that is generally unable to pay its or his liabilities as they fall due in the ordinary course of business or has liabilities that are greater than its or his assets.

To be allowed as a deduction, the value of the claim of the deceased against insolvent persons must be included in the gross estate because the claim against insolvent persons is a decedent's interest or decedent's property at the time of his death.

Monserrat v. Collector of Internal Revenue, CTA Case No. 11, December 28, 1955:

Moreover, the incapacity of the debtor to pay his obligation must be proven.

Mere allegation is not sufficient.

Unpaid Mortgage

During the lifetime of the decedent, he may incur indebtedness and use his property as a security for its payment, such as mortgage, which remains unpaid at the time of his death.

The amount of unpaid mortgage is allowed as a deduction provided the fair market value of the property mortgaged or the decedent's interest therein, undiminished by such mortgage or indebtedness, is included in the gross estate.

The deduction allowed in the case of claims against the estate, unpaid mortgages or any indebtedness is, when founded upon a promise or agreement, limited to the extent that they were contracted bona fide and for an adequate and full consideration in money or money's worth.

In case an unpaid mortgage payable is being claimed by the estate, verification must be made as to who was the beneficiary of the loan proceeds.

If the loan is found to be merely an accommodation loan where the loan proceeds went to another person, the value of the unpaid loan must be included as a receivable of the estate.

❌ If there is a legal impediment to recognize the same as receivable of the estate, said unpaid obligation/mortgage payable shall not be allowed as a deduction from the gross estate.

In all instances, the mortgaged property, to the extent of the decedent's interest therein, should always form part of the gross taxable estate.

Unpaid Taxes

To claim taxes as an allowable deduction, the taxes must have accrued as of date of death of the decedent and remain unpaid as of the time of death.

However, the following taxes cannot be claimed as deductions:

❌ Income tax upon income received after death;

❌ Property taxes not accrued before his death; or

❌ Estate tax due from the transmission of his estate.

Losses

From the date of death of the decedent and during the settlement of the estate, there are losses that may occur on the properties owned by the decedent.

Example:

When the decedent left a residential house that was consumed by fire or jewelries stolen.

These losses may be claimed as a deduction for estate tax purposes subject to the following requisites: F-CD-L

The losses are due to fires, storms, shipwreck, or other casualties, or from robbery, theft, or embezzlement;

The losses are not compensated for by insurance or otherwise;

The losses are not claimed as a deduction for income tax purposes in an income tax return, and

The losses are incurred not later than the last day for the payment of the estate tax.

TRAIN Law

Under the TRAIN Law, the filing of estate tax return is extended from six (6) months to one (1) year from the date of death of the decedent.

This also means the deadline for payment of estate tax is extended to one (1) year.

Hence, the period within which losses may be incurred is also modified from six (6) months to one (1) year.

Property Previously Taxed or Vanishing Deduction

A vanishing deduction operates to ease the harshness of successive taxation of the same property within a relatively short period to time occasioned by the untimely death of the transferee after the death of the prior decedent or after the donation.

Estate of Reyes v. Commissioner of Internal Revenue, C.T.A. Case No. 6747, January 16, 2006:

A vanishing deduction is a deduction allowed from the gross estate of citizens, resident aliens and non-resident estates for properties which were previously subject to donor's or estate taxes.

The deduction allowed diminishes for a period of five (5) years.

Simply, there are two (2) occasions where vanishing deduction may arise.

First, a decedent transferred his property to his heir/ transferee.

The transfer is subject to estate tax.

Subsequently and within a period of five (5) years, the heir/transferee who still owns the property received from the first decedent also died.

The second transfer is also subject to estate tax.

The estate in the second transfer may claim vanishing deduction as allowable deduction.

In this scenario, there is succession followed by another succession.

Second, a person donated a property to the donee.

The transfer is subject to donor's tax.

Subsequently and within a period of five (5) years, the donee who still owns the property donated died.

The second transfer is subject to estate tax.

The estate may claim vanishing deduction as allowable deduction.

In this scenario, there is donation followed by succession.

There is no vanishing deduction:

❌ if the first transfer is a donation and the second transfer is also a donation or

❌ if the first transfer is a succession and the second transfer is a donation.

Requisites to Claim Vanishing Deduction

The following are the requisites before vanishing deduction may be claimed: 5LG-DD

The present decedent died within five (5) years from the date of death of the prior decedent or the present decedent died within five (5) years from the date of donation;

The property must be located in the Philippines and can be specifically identified as the one received from the prior decedent or from the donor, or which can be identified as having been acquired in exchange for property so received;

The value of the property must be included in the gross estate of the present decedent;

The donor's tax or estate tax on the prior transfer must be finally determined and paid by or on behalf of such donor, or the estate of such prior decedent; and

The estate of the prior decedent did not claim or was not allowed to claim vanishing deduction in the case of multiple succession.

The decreasing percentages of deduction (hence the word i. "vanishing") are:

One hundred percent (100%) of the value,

if the prior decedent died within one (1) year prior to the death of the decedent, or if the property was transferred to him by gift within the same period prior to his death;

Eighty percent (80%),

if the period is more than one (1) year but not more than two (2) years;

Sixty percent (60%),

if the period is more than two (2) years but not more than three (3) years;

Forty percent (40%),

if the period is more than three (3) years but not more than four (4) years; and

Twenty percent (20%),

if the period is more than four (4) years but not more than five (5) years.

Transfer for Public Use

The amount of all the bequests, legacies, devises or transfers to or for the use of the Government of the Republic of the Philippines, or any political subdivision thereof, for exclusively public purposes is allowed as deduction as transfer for public use.

Family Home

Family home refers to the dwelling house, including the land on which it is situated, where the husband and wife, or the head of the family, and members of their family reside.

The Barangay Captain of the locality where the family home is located must issue a certification that it is actually the family home of the decedent.

The family home is deemed constituted on the house and lot from the time it is actually occupied as a family residence and is considered as such for as long as any of its beneficiaries actually resides therein.

For estate tax purposes, actual occupancy of the house or house and lot as the family residence shall not be considered interrupted or abandoned in such cases as the temporary absence from the constituted family home due to travel or studies or work abroad, etc.

In other words, the family home is generally characterized by permanency, that is, the place to which, whenever absent for business or pleasure, one still intends to return.

The family home must be part of the properties of the absolute community or of the conjugal partnership, or of the exclusive properties of either spouse depending upon the classification of the property (family home) and the property relations prevailing on the properties of the husband and wife.

It may also be constituted by an unmarried head of a family on his or her own property.

For purposes of availing of a family home deduction to the extent allowable, a person may constitute only one family home.

To claim family home as a deduction, the following conditions must be met: AG-CE

The family home must be the actual residential home of the decedent and his family at the time of his death, as certified by the Barangay Captain of the locality where the family home is situated;

The total value of the family home must be included as part of the gross estate of the decedent; and

Allowable deduction must be in an amount equivalent to the current fair market value of the family home as declared or included in the gross estate, or the extent of the decedent's interest (whether conjugal /community or exclusive property), whichever is lower, but not exceeding P1,000,000.

TRAIN Law

TRAIN Law increased the allowable amount of family home deduction from not more than P1,000,000.00 to not more than P10,000,000.00 in the settlement of estate of decedents who died January 1, 2018 onwards.

Standard Deduction

A standard deduction is a deduction without need of substantiation in the amount of One Million Pesos (P1,000,000.00).

The full amount of P1,000,000.00 is allowed as deduction for the benefit of the decedent.

The only requirement is that the decedent is either a:

✅ resident citizen,

✅ non-resident citizen, or

✅ resident alien.

TRAIN Law

Effective January 1, 2018, the standard deduction under the TRAIN Law is increased from P1,000,000.00 to P5,000,000.00.

Medical Expenses

All medical expenses (cost of medicines, hospital bills, doctors' fees, etc.) incurred (whether paid or unpaid) are allowed as deduction provided the following are present: 1-S-500

The expenses are incurred within one (1) year before the death of the decedent;

The expenses are duly substantiated with official receipts for services rendered by the decedent's attending physicians, invoices, statements of account duly certified by the hospital, and such other documents in support thereof; and

The total amount, whether paid or unpaid, does not exceed Five Hundred Thousand Pesos (P500,000).

❌ Any amount of medical expenses incurred within one year from death in excess of Five Hundred Thousand Pesos (P500,000.00) is not allowed as a deduction.

Neither can any unpaid amount thereof in excess of the P500,000.00 threshold nor any unpaid amount for medical expenses incurred prior to the one-year period from date of death be allowed to be deducted from the gross estate as a claim against the estate.

TRAIN Law

TRAIN Law repealed the provision allowing medical expense As special deduction.

Thus, estates of decedents who died on January 1, 2018 onwards may no longer claim medical expense.

Amount Received by Heirs Under Republic Act No. 4917

Any amount received by the heirs from the decedent's employer as a consequence of the death of the decedent-employee in accordance with Republic Act No. 4917 is allowed as a deduction, provided that the amount of the separation benefit is included as part of the gross estate of the decedent.

REPUBLIC ACT NO. 4917: AN ACT PROVIDING THAT RETIREMENT BENEFITS OF EMPLOYEES OF PRIVATE FIRMS SHALL NOT BE SUBJECT TO ATTACHMENT, LEVY, EXECUTION, OR ANY TAX WHATSOEVER.

Deductions to Estate of Non-Resident Alien Decedent

Under the Tax Code, the estate of a non-resident alien decedent is allowed the following deductions: EPT

Expenses, Losses, Indebtedness, and Taxes proportion of the total expenses, losses, indebtedness, and taxes which the value of such part bears to the value of his entire gross estate wherever situated is allowed as deduction.

The allowable deduction shall be computed using the following formula:

Allowable Deduction =

Gross Estate-PhilippinesGross Estate-World ELIT

Property Previously Taxed; and

Transfer for Public Use.

The estate of a non-resident alien decedent is not allowed to claim special deductions such as family home, medical expenses, standard deduction, and benefits received under Republic Act No. 4917.

TRAIN Law:

Upon the effectivity of the TRAIN Law, funeral and judicial expenses are removed from the list of ordinary deductions.

This means the proportion of the total expenses now excludes these expenses.

However, the estate of a non-resident alien decedent can still claim the proportion of losses, indebtedness, and taxes.

Significantly, TRAIN Law now allows the estate of a non resident alien decedent to claim standard deduction in the amount of P500,000.00.

Net Share of the Surviving Spouse in the Conjugal Partnership or Community Property

After deducting the allowable deductions appertaining to the conjugal or community properties included in the gross estate, the share of the surviving spouse must be removed to ensure that only the decedent's interest in the estate is taxed.

Tax Credit for Estate Taxes Paid in a Foreign Country

The estate of citizen and resident decedents are taxable in all their properties located within or without the Philippines.

Through this, it is possible that their properties outside the Philippines are also taxable in the foreign country where these properties are located.

In order to avoid or at least minimize the effect of double taxation, an estate tax credit on the estate taxes paid in a foreign country is allowed in the Philippines.

Limitations on Tax Credit

The estate tax credit that may be allowed in the Philippines is subject to the following limitations:

The amount of the credit in respect to the tax paid to any country shall not exceed the same proportion of the tax against which such credit is taken, which the decedent's net estate situated within such country taxable under this Title bears to his entire net estate; and

The total amount of the credit shall not exceed the same proportion of the tax against which such credit is taken, which the decedent's net estate situated outside the Philippines taxable under the Tax Code to his entire net estate.

In fine, the tax credit allowed shall depend on whether one foreign country or multiple foreign countries are involved.

One Foreign Country

The tax credit is whichever is lower of the actual estate tax paid in foreign country and the limit as determined below:

Limitation =

Net Taxable Estate-ForeignNet Taxable Estate-World Estate Tax Due

Multiple Foreign Countries

Determine whichever is lower of the actual estate tax paid in each of the foreign country and the limit per country using the formula above.

Determine the total world estate tax credit limit using the formula below:

Limitation =

Net Taxable Estate-ForeignNet Taxable Estate-World Estate Tax Due

The allowable estate tax credit is whichever is lower between the computed limitations in items 1 and 2 above.

Estate Tax Administration

Notice of Death

Under the Tax Code, the executor, administrator, or any of the legal heirs of the decedent must inform the BIR, through the Commissioner, of the fact of death of the decedent.

This is accomplished by filing a notice of death to the BIR.

The notice of death is required in all cases where the transfer is subject to tax or where the transfer, though exempt, the gross value of the estate exceeds P20,000.00.

The notice of death must be filed within two (2) months after the decedent's death, or within a like period after qualifying as such executor or administrator.

Failure to file a notice of death within the period prescribed makes the estate liable to corresponding penalty.

TRAIN Law:

Under the TRAIN Law, the requirement of notice of death is removed.

Estate Tax Returns

The estate tax return (BIR Form No. 1801) must be filed in the following instances: T-200-R

In all cases of transfers subject to estate tax;

In cases, though exempt from tax, where the gross value of the estate exceeds P200,000.00; or

In cases regardless of the gross value of the estate, where the said estate consists of registered or registrable property such as real property, motor vehicle, shares of stock or other similar property for which a clearance from the BIR is required as a condition precedent for the transfer of ownership.

TRAIN Law:

Under the TRAIN Law, deleted in Section 90(A) of the NIRC is the phrase "or where, though exempt from tax, the gross value of the estate exceeds Two hundred thousand pesos (P200,000)" emphasizing the need to file an estate tax return of the subject estate regardless of the value of the estate.

Contents of the Estate Tax Return

The Estate Tax Return, which is filed under oath and in duplicate, shall contain the following information: VDA

The value of the gross estate of the decedent at the time of his death, or in case of a non-resident, not a citizen of the Philippines, of that part of his gross estate situated in the Philippines;

The deductions allowed from gross estate in determining the estate; and

Such part of such information as may at the time be ascertainable and such supplemental data as may be necessary to establish the correct taxes.

Certification by a Certified Public Accountant

A certification by a Certified Public Accountant (CPA) is required as a supporting document to the estate tax return when the gross value of the estate exceeds P2,000,000.00.

The certification shall also contain: ADA

Itemized assets of the decedent with their corresponding gross value at the time of his death, or in the case of a non-resident, not a citizen of the Philippines, of that part of his gross estate situated in the Philippines;

Itemized deductions from gross estate allowed in Section 86 of the NIRC; and

The amount of tax due whether paid or still due and outstanding.

TRAIN Law:

Under the TRAIN Law, the amount of gross value of estate provided in the estate tax return that must be supported by a statement duly certified by a CPA is increased from P2,000,000.00 to P5,000,000.00.

Time for Filing of Estate Tax Return and Its Extension

Under the Tax Code, the estate tax return must be filed within six (6) months from the decedent's death.

The Commissioner has the authority to grant, in meritorious cases, a reasonable extension not exceeding thirty (30) days for filing the return.

The court approving the project of partition shall furnish the Commissioner with a certified copy thereof and its order within thirty (30) days after promulgation of such order.

TRAIN Law:

Under the TRAIN Law, the deadline for filing of estate tax return is extended from six (6) months to one (1) year from the date of death of the decedent.

Time of Payment of Estate Tax

In the Philippines, the BIR adopts the pay-as-you-file system which means the deadline for payment of tax is on the deadline of the filing of the corresponding tax return.

Thus, the estate tax is paid at the time the estate tax return is filed by the executor, administrator or the heirs, i.e., which is within six (6) months from the date of death of the decedent.

TRAIN Law:

Under the TRAIN Law, considering the deadline for filing of the return is extended, payment of estate tax is also extended from six (6) months to one (1) year from the date of death.

Extension of Payment of Estate Tax

The payment of estate tax may be extended when the Commissioner finds that the payment on the due date of the estate tax or of any part thereof would impose undue hardship upon the estate or any of the heirs.

The extension for payment of estate tax depends on whether the estate is settled judicially or extra-judicially.

In case of judicial settlement, the payment of estate tax may be extended for a period not exceeding five (5) years.

In case of extra-judicial settlement, the payment may be extended to a period not exceeding two (2) years.

Any amount paid after the statutory due date of the tax, but within the extension period, is subject to interest but not to surcharge.

If an extension is granted, the Commissioner may require the executor, or administrator, or beneficiary, as the case may be, to furnish a bond in such amount, not exceeding double the amount of the tax and with such sureties as the Commissioner deems necessary, conditioned upon the payment of the said tax in accordance with the terms of the extension.

❌ vThere is no extension for payment of taxes which may be granted by the Commissioner where the taxes are assessed by reason of negligence, intentional disregard of rules and regulations, or fraud on the part of the taxpayer.

Effect of Extension of Payment

In the event that the payment of estate tax is extended, the estate tax must be paid on or before the date of the expiration of the period of the extension.

In addition, the running of the Statute of Limitations for assessment as provided in Section 203 of the NIRC or the period of the government to assess is suspended for the period of any such extension.

Sec. 203. Period of Limitation Upon Assessment and Collection.

Except as provided in Section 222, internal revenue taxes shall be assessed within three (3) years after the last day prescribed by law for the filing of the return, and no proceeding in court without assessment for the collection of such taxes shall be begun after the expiration of such period:

Provided, That in a case where a return is filed beyond the period prescribed by law, the three (3)-year period shall be counted from the day the return was filed. For purposes of this Section, a return filed before the last day prescribed by law for the filing thereof shall be considered as filed on such last day.

Payment of the Estate Tax by Installment

In case the available cash of the estate is not sufficient to pay its total estate tax liability, the estate may be allowed to pay the tax by installment and a clearance shall be released only with respect to the property the corresponding/computed tax on which has been paid.

There shall, therefore, be as many clearances (Certificates Authorizing Registration) as there are as many properties released because they have been paid for by the installment payments of the estate tax.

The computation of the estate tax, however, shall always be on the cumulative amount of the net taxable estate.

Any amount paid after the statutory due date of the tax shall be imposed the corresponding applicable penalty thereto.

However, if the payment of the tax after the due date is approved by the Commissioner or his duly authorized representative, the imposable penalty thereon shall only be the interest.

Nothing in this paragraph, however, prevents the Commissioner from executing enforcement action against the estate after the due date of the estate tax provided that all the applicable laws and required procedures are followed/observed.

TRAIN Law:

The TRAIN Law inserted an additional provision which provides for payment by installment in case the available cash of the estate is insufficient to pay the total estate tax due.

Payment shall be allowed within two (2) years from the statutory date for its payment without civil penalty and interest.

Place of Filing of Estate Tax Return and Place of Payment

In case of a resident decedent, whether citizen or alien, the administrator or executor shall register the estate of the decedent and secure a new TIN from the Revenue District Office where the decedent was domiciled at the time of his death and shall file the estate tax return and pay the corresponding estate tax with the:

Accredited Agent Bank (AAB),

Revenue District Officer,

Collection Officer or

duly authorized Treasurer of the city or municipality where the decedent was domiciled at the time of his death, whichever is applicable.

In case of a non-resident decedent, whether non-resident citizen or non-resident alien, with executor or administrator in the Philippines, the estate tax return shall be filed with and the TIN for the estate shall be secured from the Revenue District Office where such executor or administrator is registered.

In case the executor or administrator is not registered, the estate tax return shall be filed with and the TIN of the estate shall be secured from the Revenue District Office having jurisdiction over the executor or administrator's legal residence.

Nonetheless, in case the non-resident decedent does not have an executor or administrator in the Philippines, the estate tax return shall be filed with and the TIN for the estate shall be secured from the Office of the Commissioner through RDO No. 39-South Quezon City.

The Commissioner of Internal Revenue is authorized to exercise his power to allow a different venue/place in the filing of tax returns.

Withdrawal of Bank Deposits

If a bank has knowledge of the death of a person, who maintained a bank deposit account alone, or jointly with another, the bank cannot allow any withdrawal from the said deposit account, unless the Commissioner has certified that the estate tax is paid.

A certification issued by the Commissioner is required before the bank can allow withdrawal of bank deposits.

As an exception, the administrator of the estate or any one (1) of the heirs of the decedent may, upon authorization by the Commissioner, withdraw an amount not exceeding P20,000.00 without the said certification.

For this purpose, all withdrawal slips shall contain a statement to the effect that all of the joint depositors are still living at the time of withdrawal by any one (1) of the joint depositors and such statement shall be under oath by the said depositors.

TRAIN Law:

TRAIN Law removes the P20,000.00 limit on bank withdrawal without certification from the BIR.

Even without certification, TRAIN Law now allows for the withdrawal of any amount, but subject to a final withholding tax of six percent (6%).

However,the withdrawal shall only be made within one (1) year from the date of death of the decedent.

Summary of Changes Under the Train Law

TRAIN Law or Republic Act No. 10963 took effect on January 1, 2018.

It modified and repealed some provisions of the NIRC.

The following are the changes brought by TRAIN Law in estate tax:

Estate Tax Rate

TRAIN Law simplifies the estate tax schedule, from a six bracket schedule with rates ranging from five to twenty percent (5%- 20%), to a single rate of six percent (6%) based on the value of the net estate.

A flat rate of six percent (6%) now applies regardless of the amount of the net estate of every decedent, whether resident or non resident of the Philippines.

This means that the first P200,000.00 net taxable estate under the Tax Code is no longer exempt and now subject to six percent (6%) estate tax.

Deductions Allowed to Citizen and Resident Decedents

Removal of Expenses as Deduction

Under the TRAIN Law, the following are no longer allowed as a deduction: AJM

actual funeral expense

judicial expense and

medical expense

Increase of Standard Deduction

In lieu of the expenses, the standard deduction is increased from P1,000,000.00 to P5,000,000.00.

Family Home

The amount of deduction for family home is increased from not more than P1,000,000.00 to not more than P10,000,000.00.

It must be noted that TRAIN Law removed as a sine qua non condition that the family home must have been the decedent's family home as certified by the barangay captain of the locality before one may claim it as an exemption or deduction.

However, Revenue Regulations No. 12-2018 was issued to implement the provisions of the TRAIN Law pertaining to estate tax retains such requirement.

Summary of Deductions

In summary, the deductions allowed to citizen and resident decedents are:

Ordinary Deductions LPT

Losses, Indebtedness, Taxes (LIT)

Losses

Claims Against the Estate

Claims Against Insolvent Person

Unpaid Mortgage

Unpaid Taxes

Property Previously Taxed or Vanishing Deduction; and

Transfer for Public Use

Special Deductions FBS

Family Home (maximum of P10,000,000.00)

Benefits Received under Article 4917

Standard Deduction (P5,000,000.00)

Deductions Allowed to Non-Resident Decedents

Standard Deduction for Non-Resident Alien Decedent

A non-resident alien decedent is not allowed to claim actual funeral expenses and judicial expenses.

Instead, a non-resident alien decedent is allowed to claim standard deduction of P500,000.00 without substantiation.

Deductions on Pro-Rated Basis by Non-Resident Alien Decedent

For a non-resident alien who claims expenses on a pro-rated basis, the actual funeral expense and judicial expense are no longer included in the deductions he can claim pro-rata.

Thus, the pro-rated deductions now only include: CCUUC

claims against the estate,

claims against insolvent person,

unpaid mortgage,

unpaid taxes, and

casualty losses.

Requirement of Non-Resident Alien to Claim Deduction

Prior to TRAIN Law, in Section 86(D) of the NIRC, it was required that the executor, administrator, or any one of the heirs shall include in the estate tax return that part of the nonresident alien's gross estate not situated in the Philippines to be able to claim deductions.

This requirement is removed by TRAIN Law.

Summary of Deductions

In summary, the deductions allowed to non-resident decedents are:

Ordinary Deductions LPTS

Losses, Indebtedness, Taxes (LIT) (Pro-rated only)

Losses

Claims Against the Estate

Claims Against Insolvent Person

Unpaid Mortgage

Unpaid Taxes

Property Previously Taxed or Vanishing Deduction;

Transfer for Public Use; and

Standard Deduction (P500,000.00)

Estate Tax Administration

Notice of Death

Filing of notice of death is no longer required.

Filing of Estate Tax Return

Deleted in Section 90(A) of the NIRC is the phrase "or where, though exempt from tax, the gross value of the estate exceeds Two hundred thousand pesos (P200,000)", emphasizing the need to file an estate tax return of the subject estate.

Certification by a Certified Public Accountant

The amount of gross value of estate provided in the estate tax return that must be supported by a statement duly certified by a CPA is increased from P2,000,000.00 to P5,000,000.00.

Deadline for Filing of Estate Tax Return

The deadline for filing of estate tax return is extended from six (6) months to one (1) year from the date of death of the decedent.

Due to this change on the deadline of filing of estate tax return, the deadline for payment is also extended from six (6) months to one (1) year.

In Addition, recall that one of the requirements to claim "losses" as deduction from the gross estate is that the "losses" are incurred not later than the last day for the payment of the estate tax.

Due to the extension of the deadline for payment of estate tax, the period within which the "losses" must be incurred is also extended to one (1) year.

Payment of Estate Tax by Installment

An additional provision is inserted which provides for the payment by installment in case the available cash of the estate is insufficient to pay the total estate tax due.

Payment shall be allowed within two (2) years from the statutory date for its payment without civil penalty and interest.

Withdrawal of Bank Deposits

The TRAIN Law removes the P20,000.00 limit on bank withdrawal without certification from the BIR.

Even without certification, TRAIN Law now allows for the withdrawal of any amount but subject to a final withholding tax of six percent (6%).

However, the withdrawal shall only be made within one (1) year from the date of death of the decedent.