Basic Taxation Law: Donor's Tax

Donor’s Tax

Preliminary

Donation

Article 725, New Civil Code:

Donation is an act of liberality whereby a person disposes gratuitously of a thing or right in favor of another, who accepts it.

Spouses Romulo and Sally Eduarte u. Court of Appeals,G.R. No. 105944, February 9, 1996:

On the part of the donor, it is an exercise of one's generosity.

For tax purposes, donation may be donation mortis causa or donation inter vivos.

Donation mortis causa is a donation that takes effect upon the death of the donor.

This donation is subject to estate tax.

Donation inter vivos, on the other hand, is a donation made between living persons or those to take effect during the lifetime of the donor.

This donation is subject to donor's tax.

Republic of the Philippines v. David Rey Guzman, G.R. No. 132964, February 18, 2000:

Donation has the following elements: RII

the reduction of the patrimony of the donor;

the increase in the patrimony of the donee; and,

the intent to do an act of liberality or animus donandi.

Essential Requisites of Donation

In order to be valid, a donation must have the following essential requisites:

CD-AD

Capacity of the Donor

The donor must have the capacity to donate which is determined as of the time of the making of the donation.

All persons who may contract and dispose of their property may make a donation.

Donative Intent

It refers to the intent of the donor to make a gift.

Donative intent is necessary only in cases of direct gift.

If the gift is indirectly taking place by way of sale, exchange, or other transfer of property as contemplated in cases of transfers for less than adequate and full consideration in Section 100 of the Tax Code, intent to donate is not essential to constitute a gift.

Donative intent is presumed present when one gives a part of one's patrimony to another without consideration.

Acceptance of the Donee

The transfer of property by gift is perfected from the moment the donor knows of the acceptance by the donee.

Delivery of the Gift

Delivery of gift, whether actual or constructive, of the donated property to the donee completes the donation.

Formal Requisites of Donation

In addition to the essential requisites, a donation must comply with formal requisites for its validity.

The form of a donation depends on the property involved.

Movable Property

The donation of a movable property may be made orally or in writing.

A movable property with a value not exceeding P5,000.00 can be made orally.

However, an oral donation requires the simultaneous delivery of the thing or of the document representing the right donated.

If the value of the movable property donated exceeds P5,000.00, the donation and the acceptance shall be made in writing. Otherwise, the donation shall be void.

Immovable Property

If the donation involves immovable property, the donation must be in a public instrument, specifying therein the property donated and the value of the charges which the donee must satisfy.

The acceptance of donation by the donee must also be in a public instrument either in the same deed of donation or in a separate public document.

The acceptance shall not take effect unless it is done during the lifetime of the donor.

If the acceptance is made in a separate instrument, the donor shall be notified thereof in an authentic form, and this step shall be noted in both instruments.

A donation of immovable property that does not comply with the required form as stated above is a void and inexistent donation.

In donation of immovable property, the value of the property donated is irrelevant.

Regardless of its value, a donation of immovable property must be in a public instrument to be valid.

The value of property donated is relevant only with respect to movable property.

Donor’s Tax

Donor's tax is a transfer tax levied, assessed, collected, and paid upon the transfer of any person, resident or non-resident, of the property by gift inter vivos.

It applies whether the transfer is in trust or otherwise, whether the gift is direct or indirect, and whether the property is real or personal, tangible or intangible.

Nature of Donor's Tax and the Law That Governs the Imposition of Donor's Tax

A donor's tax is a tax on the privilege of transmitting one's property or property rights to another or others without adequate and full valuable consideration.

It is an excise tax on the privilege of the donor to give or on the transfer of property by way of gift inter vivos.

Rev. Fr. Casimiro Lladoc v. Commissioner of Internal Revenue, G.R. No. L-19201, June 16, 1965:

The donor's tax is not a property tax, but is a tax imposed on the transfer of property by way of gift inter vivos.

The donor's tax shall not apply unless and until there is a completed gift.

The transfer of property by gift is perfected from the moment the donor knows of the acceptance by the donee; it is completed by the delivery, either actually or constructively, of the donated property to the donee.

Thus, the law in force at the time of the perfection/completion of the donations shall govern the imposition of the donor's tax.

Purpose or Object of Donor's Tax

Donor's tax supplements the estate tax by preventing the avoidance of the latter through the device of donating the property during the lifetime of the deceased.

It also prevents the avoidance of income taxes.

Without the donor's tax, the donor may escape the progressive rates of income taxation through the simple expedient of splitting his income amount numerous donees.

Transfers and Transactions Constituting Donation

There are certain transfers that constitute donation or transactions that result to donation, and thus, may be subject to donor’s tax. CCRRT

Campaign Contributions

Cancellation of Indebtedness

Renunciation of Inheritance

Renunciation of the Surviving Spouse of the Share in the Conjugal Partnership or Absolute Community

TransferforLess ThanAdequate andFull Consideration

1. Campaign Contributions

Any contribution in cash or in kind to any candidate, political party or coalition of parties for campaign purposes shall be governed by the Election Code, as amended.

❌ Under Section 13 of Republic Act No. 7166, any contribution in cash or in kind to any candidate or political party or coalition of parties for campaign purposes, duly reported to the Commission on Elections (COMELEC), is not subject to the payment of any gift tax, thus, exempt from donor's tax.

However, only those donations/contributions that have been utilized/spent during the campaign period as set by the COMELEC are exempt from donor's tax.

✅ Donations utilized before or after the campaign period are subject to donor's tax and not deductible as political contribution on the part of the donor.

Donation or contribution in cash or in kind to any candidate, political party or coalition of parties has also income tax consequences.

❌ As a general rule, campaign contributions are not included in the taxable income of the candidate to whom they were given.

This is because such contributions were given not for the personal expenditure/enrichment of the concerned candidate but for the purpose of utilizing such contributions for his campaign.

Thus, to be considered as exempt from income tax, these campaign contributions must be utilized to cover a candidate's expenditures for his electoral campaign.

✅ Unutilized or excess campaign funds are subject to income tax and as such, must be included in the candidate's taxable income.

Any losing or winning candidate who fails to file with the COMELEC the appropriate Statement of Expenditures is precluded from claiming such expenditures as deductions from his contributions.

In such case, the entire amount of such campaign contributions is considered as subject to income tax.

2. Cancellation of Indebtedness

The cancellation and forgiveness of indebtedness may amount to a: PGC

payment of income,

to a gift, or

to a capital transaction, depending upon the circumstances.

Subject to Income Tax:

If an individual performs services for a creditor, who, in consideration of the services cancels the debt, income to that amount is realized by the debtor as compensation for his services.

In this case, the debtor who is the income earner is subject to income tax.

Increase in Assets:

It has been settled that before a condonation or forgiveness of indebtedness will give rise to a taxable income, there must be an increase in the assets of the debtor thereby enriching the latter.

❌ A transaction whereby nothing of exchangeable value comes to or is received by a taxpayer does not give rise to or create a taxable income.

✅ Gain or profit is essential to the existence of taxable income.

❌ Thus, if one condones the debt of another who remains insolvent before and after the said condonation, such condonation shall not be subject to income tax.

❌ Moreover, the condonation is likewise not subject to gift tax since there is no donative intent but solely for business consideration.

✅ If a creditor merely desires to benefit a debtor and without any consideration therefor cancels the debt, the amount of the debt is a gift from the creditor to the debtor.

In this case, the creditor is the donor who is liable to donor's tax.

On the part of the debtor who is the donee, the debt cancelled need not be included in his gross income for income tax purposes.

Corporation Dividend:

If a corporation to which a stockholder is indebted forgives the debt, the transaction has the effect of the payment of a dividend.

In this case, the cancellation of debt treated as declaration of dividends may be subject to income tax.

3. Renunciation of Inheritance

The heirs of the decedent, including the surviving spouse, may renounce his/her share in the inheritance or hereditary estate left by the decedent.

Renunciation may either be general renunciation or special renunciation.

General renunciation is a refusal to receive inheritance or hereditary estate in favor of no specifically identified heir.

❌ General renunciation by an heir of his/her share in the inheritance or hereditary estate is not subject to donor's tax.

Special renunciation is a refusal to receive inheritance or hereditary estate specifically and categorically done in favor of identified heir/s to the exclusion or disadvantage of the other co-heirs in the hereditary estate.

✅ Special renunciation is subject to donor's tax.

4. Renunciation of the Surviving Spouse of the Share in the Conjugal Partnership orAbsolute Community

After the dissolution of marriage due to death, the surviving spouse may choose to receive or renounce his/her share in the conjugal partnership or absolute community.

✅ The renunciation of the surviving spouse of his/her share in the conjugal partnership or absolute community after the dissolution of marriage in favor of the heirs of the deceased spouse or any other person/s is subject to donor's tax.

Renunciation of the surviving spouse of the share in the conjugal partnership or absolute community is subject to donor's tax regardless of the type of renunciation whether general or special.

5. Transfer for Less Than Adequate and Full Consideration

Transfer for less than adequate and full consideration in money or money's worth is an example of indirect donation where donative intent is not necessary.

In indirect donation, the person transferring a property to another is contemplating a transaction, i.e., sale transaction, but the circumstances present and surrounding the transaction made the transaction a donation.

When a property is sold, the fair market value of the property at the time of execution of the contract to sell or deed of absolute sale is compared with the agreed or actual consideration or the selling price as stated in the said contract to sell or deed of absolute sale.

The sale is said to be for less than adequate and full consideration when the fair market value is higher than or exceeded the agreed or actual consideration or the selling price.

In this case, the excess of the fair market value over the consideration is “deemed gift” and shall be included in computing the amounts of gifts made during the calendar year.

Deemed Gift = Fair Market Value of the Property at the Time of the Execution - Agreed or Actual Consideration

❌ The above rule on “deemed gift” does not apply to real properties classified as capital assets subject to final income tax under Section 24(D)(1) of the Tax Code.

It is clear that “deemed gift” is intended to impose donor's tax on the difference of the fair market value and the consideration of the sale that is not captured in the imposition of income tax because the gain, for income tax purposes, is computed by deducting the acquisition cost of the property from the consideration or selling price.

Gain = Selling Price - Acquisition Cost

In this case, fair market value is ignored.

This is not the case of a real property classified as capital asset because the capital gains tax of six percent (6%) is imposed on the fair market value or gross selling price, whichever is higher.

Thus, the full amount of fair market value is captured for income tax purposes.

Prior to enactment of TRAIN Law, Section 100 of the Tax Code read as follows:

SEC. 100. Transfer for Less Than Adequate and Full Consideration. Where property, other than real property referred to in Section 24(D), is transferred for less than an adequate and full consideration in money or money's worth, then the amount by which the fair market value of the property exceeded the value of the consideration shall, for the purpose of the tax imposed by this Chapter, be deemed a gift, and shall be included in computing the amount of gifts made during the calendar year.

The legislative intendment of the “deemed gift” provision under Section 100 of the Tax Code is to discourage the parties to a sale from manipulating their selling price in order to save on income taxes.

This is because, under the Tax Code, the measurement of gain from a disposition of properties merely considers the amount realized from the sale, which is the selling price minus the basis of the property sold.

Hence, if the parties would declare a lower selling price per document of sale than the actual amount of money which changed hands, there is foregone revenue and the government is placed at a very disadvantageous position.

In order to plug this tax leakage, Section 100 automatically treats the disparity between the fair market value and selling price of the property as gift subject to donor's tax.

In short, the "deemed gift" provision compliments the income tax rule on the measurement of gain and accordingly, works to about recurrence of under declaration of the selling price.

Thus, if the fair market value of the shares of stock is higher than the selling price, the excess/difference shall be treated as gift subject to donor's tax.

The Philippine American Life and General Insurance Company v. Secretary of Finance, et al. (G.R. No. 210987, November 24, 2014):

The Supreme Court ruled that the absence of donative intent, if that be the case, does not exempt the sales of stocks transaction from donor's tax since Section 100 of the NIRC categorically states that the amount by which the fair market value of the property exceeded the value of the consideration shall be deemed a gift.

Thus, even if there is no actual donation, the difference in price is considered a donation.

The TRAIN Law which took effect on January 1, 2018, however, provides an exception.

Section 100 of the Tax Code now further states that:

Provided, however, that a sale, exchange, or other transfer of property made in the ordinary course of business (a transaction which is a bona fide, at arm's length, and free from any donative intent), will be considered as made for an adequate and full consideration in money or money's worth.

Under the rules on statutory construction, exceptions, as a general rule, should be strictly, but reasonably construed; they extend only so far as their language fairly warrants, and all doubts should be resolved in favor of the general provisions rather than the exception.

The appropriate and natural office of the exception is to exempt something from the scope of the general words of a statute, which is otherwise within the scope and meaning of such general words.

Consequently, the existence of an exception in a statute clarifies the intent that the statute shall apply to all cases not excepted.

Exceptions are subject to the rule of strict constructions; hence, any doubt will be resolved in favor of the general provision and against the exception.

Indeed, the liberal construction of a statute will seem to require in many circumstances that the exception, by which the operation of the statute is limited or abridged, should receive a restricted construction.

Thus, starting January 1, 2018, when shares of stock not traded in stock exchange are sold for less than its fair market value, the excess of the fair market value over the selling price shall be treated as gift subject to donor's tax imposed by Section 100 of the Tax Code, as amended, except when it is sold at arm's length, free from any donative intent in the ordinary course of business.

The determination of whether the sale of shares of stock not listed and traded is at arm's length is a question of fact and not of law.

Since an arm's length transaction is a question of fact, it therefore behooves upon the party seeking to apply the exception to prove that indeed the sale involves no irregularity between unrelated and independent parties.

This would require presentation and reception of reasonable evidence sufficient enough to convince that the sale of the shares of stock for less than its fair market value is without intent to evade and defraud the government (of the tax due therein).

The evidence that should be presented should be viewed in accordance with its relation and relevance to the transaction on a case to case basis.

An arm's length sale refers to a transaction between two independent parties acting in their own best interests, without undue influence or pressure from the other side.

Donor’s Tax Liability

The donor's tax is computed by multiplying the appropriate donor's tax rate with the net taxable gift which is its tax base.

“Net gift” is the net economic benefit from the transfer that accrues to the donee.

The donor is the statutory taxpayer of donor's tax.

In general, the donor's tax is computed as follows:

Net Taxable Gift = Gross Gift - Deductions

Donor’s Tax Due = Net Taxable Gift x Donor's Tax Rate

Donor’s Tax Still Due = Donor’s Tax Due - Tax Credits

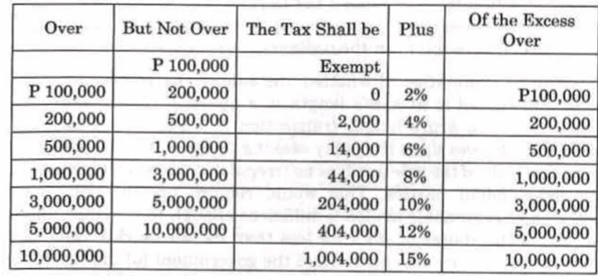

Under the Tax Code, the donor's tax rate is determined based on who the donee is, whether a relative or stranger.

A relative of the donor is a person who is: BSSAL-CCL4

a brother, sister (whether by whole or half-blood), spouse, ancestor and lineal descendant; or

a relative by consanguinity in the collateral line within the fourth degree of relationship.

Any person not falling in the definition of a relative is considered a stranger.

When the donee is a stranger, the tax payable by the donor shall be thirty percent (30%) of the net gifts.

On the other hand, if the donee is a relative, the following graduated and progressive rates apply:

From the above schedule, the first P100,000.00 net gift is exempt from donor's tax when the donee is a relative.

However, this exemption is not applicable when the donee is a stranger because a rate of thirty percent (30%) applies regardless of the value of the net gift.

TRAIN Law:

Upon the effectivity of the TRAIN Law, the donor's tax rates are modified.

The tax for each calendar year shall be six percent (6%) computed on the basis of the total net gifts in excess of P250,000.00 exempt gift made during the calendar year.

The TRAIN Law does not anymore distinguish who the donee is and a flat rate of six percent (6%) applies both to a relative and stranger.

Moreover, the six percent (66) donor's tax rate is in excess of P250,000.00 net gift making the first P250,000.00 exempt from donor's tax.

Determination and Composition of Gross Gift

Gross gift refers to the value of the property or right donated or transferred by the donor to the donee before any deduction.

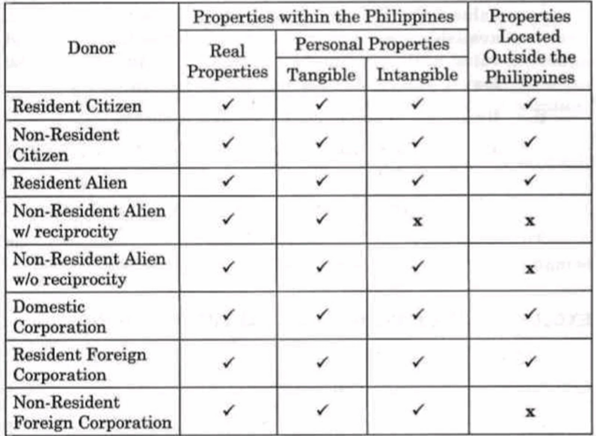

The properties included in the gross gift or those subject to donor's tax are determined based on: CLR

the classification of the donor,

the location of the property, and

whether the reciprocity rule applies.

Classification of Donor

Donor may either be a natural person or a juridical person.

Unlike in estate tax, juridical person may be a donor or a donee.

It is important to determine the classification of donor to ascertain whether the properties donated are subject to donor's tax or not.

The donor may be classified as follows: CRA-NRA-DRFC-NRFC

Citizen and Resident Alien

The citizen and resident alien donors are subject to donor's tax regardless of where the gift is made or where the property donated is located.

In short, these donors are taxable in all properties donated within and without the Philippines.

Non-Resident Alien

Non-resident alien donors are subject to donor's tax only on their donations of properties located in the Philippines, subject to the reciprocity rule.

Domestic and Resident Foreign Corporation

As juridical persons, domestic and resident foreign corporations may donate properties.

Domestic and resident foreign corporation donors are subject to donor's tax regardless of where the gift is made or where the property donated is located.

In short, they are taxable for all properties donated within and without the Philippines.

Non-Resident Foreign Corporation

Non-resident foreign corporation donors are subject to donor's tax only on its donations of properties located in the Philippines.

Unlike non- resident alien donors, the reciprocity rule does not apply to non-resident foreign corporations.

Reciprocity Rule

A non-resident alien donor is taxable only on properties, real and personal, situated in the Philippines.

Personal properties may either be tangible or intangible.

The inclusion of intangible personal properties in the gross grift of the non-resident alien donor depends on whether the reciprocity rule applies.

The reciprocity rule only applies to a non-resident alien donor and only on his intangible personal properties located in the Philippines.

The Reciprocity rule provides that no donor's tax will be collected in respect of intangible personal property in the following instances:

if the donor at the time of donation was a citizen and resident of a foreign country which at the time the gift is made did not impose donor's tax, in respect of intangible personal property of citizens of the Philippines not residing in that foreign country, or

if the laws of the foreign country of which the donor was a citizen and resident at the time of donation allows a similar exemption from transfer or donor's taxes of every character or description in respect of intangible personal property owned by citizens of the Philippines not residing in that foreign country.

The reciprocity rule is by nature a form of exemption from donor's tax because if the non-resident alien can avail of it, the intangible personal property will not be included in the gross gift and therefore not subject to donor's tax.

Section 104 of the Tax Code provides the intangible personal a. b properties deemed located in the Philippines, to wit: F-C85A-P

Franchise exercised in the Philippines;

Shares, obligations, or bonds issued by any corporation or sociedad anonima organized or constituted in the Philippines in accordance with its laws;

Shares, obligations or bonds by any foreign corporation eighty-five percent (85%) of the business of which is located in the Philippines;

Shares, obligations or bonds issued by any foreign corporation if such shares, obligations, or bonds have acquired a business situs in the Philippines; and

Shares or rights in any partnership, business, or industry established in the Philippines.

Note that before the reciprocity rule may apply, a donor must be citizen and resident of a foreign country that does not impose donor's tax or grants exemption thereto.

If a donor is a citizen of one foreign country buta resident of another foreign country at the time of donation, the reciprocity rule cannot be applied.

The properties included in the gross gift of different types of donor are summarized as follows:

Valuation of Gross Gift

The rules applicable in the valuation of gross estate for estate tax purposes also apply to valuation of gross gift for donor's tax purposes.

Thus, the properties comprising the gross gift are valued based on their fair market value at the time of donation.

Cash

cash gifts are valued at face amount

Personal properties

the fair market value of the personal property at the time of gift is considered as the amount of gift.

Real Property

if the property is real property, the fair market value is whichever between:

The fair market value as determined by the Commissioner of Internal Revenue, usually called the Zonal Value, and

The fair market value as shown in the schedule of values fixed by the provincial and city assessors.

Shares of Stocks

If the share is listed in the stock exchange, the fair market value is the price quote on the date of death.

If there is no available price quote on the date of death, the fair market value is the arithmetic mean between the highest and lowest quotation at a date nearest the date of death.

If the share is unlisted in the stock exchange:

Unlisted common shares are valued based on their book value; and

Unlisted preferred shares are valued at par value.

The reckoning point for valuation is the date when the donation is made.

Exclusions in Gross Gift and Exempt Donations

The following donations are exempt from donor's tax:

In the Case of Gifts Made by a Resident.

DNE

Dowries or gifts made on account of marriage and before its celebration or within one year thereafter by parents to each of their legitimate, recognized natural, or adopted children to the extent of the first Ten thousand pesos (P10,000.00);

Dowry in the amount of P10,000.00 is on a per parent per child basis.

The time period of one year applies only when the gift is given after the marriage. There is no time period restriction if the gift is given prior to the celebration of marriage.

Effective January 1, 2018, dowry is removed by TRAIN Law as an exempt donation.

Nonetheless, if the gift or dowry does not exceed the exemption limit of P250,000.00, it may still be exempted from donor's tax.

Gifts made to or for the use of the National Government or any entity created by any of its agencies which is not conducted for profit, or to any political subdivision of the said Government; and

Gifts in favor of an educational and/or charitable, religious, cultural or social welfare corporation institution, accredited non government organization, trust or philanthropic organization, or research institution or organization.

For the purpose of this exemption,a “non-profited educational and/or charitable corporation, institution, accredited nongovernment organization, trust or philanthropic organization and/or research institution or organization” is:

a school, college or university and/or charitable corporation, accredited nongovernment organization, trust or philanthropic organization and/or research institution or organization;

incorporated as a non-stock entity;

paying no dividends;

governed by trustees who receive no compensation; and

devoting all its income, whether students fees or gifts, donation, subsidies or other forms of philanthropy, to the accomplishment and promotion of the purposes enumerated in its Articles of Incorporation.

Moreover, the donee must not use more than thirty percent (30%) of the gifts for administration purposes.

In the Case of Gifts Made by a Non-resident not a Citizen of the Philippines.

NE

Gifts made to or for the use of the National Government or any entity created by any of its agencies which is not conducted for profit, or to any political subdivision of the said Government; and

Gifts in favor of an educational and/or charitable, religious, cultural or social welfare corporation, institution, foundation, trust or philanthropic organization or research institution or organization: Provided, however, that not more than thirty percent (30%) of said gift shall be used by such donee for administration purposes.

In addition, donations to the following entities are exempt from donor's tax by virtue of special laws: PIIR-UPD-GBN

Philippine Red Cross;

Integrated Bar of the Philippines;

International Rice Research Institute;

Ramon MagsaysayAward Foundation;

University of the Philippines;

Philippine Normal University;

Development Academy of the Philippines;

Girls Scout of the Philippines;

Boy Scout of the Philippines; and

National Commission for Culture and the Arts.

Deductions Allowed

Donor's tax has limited deductions allowed such as: ED

encumbrance assumed by the donee and

diminutions.

When the property donated is the subject of an encumbrance like a mortgage, the amount of unpaid mortgage may be claimed as a deduction if assumed by the donee.

If the donee does not assume the unpaid mortgage, then it is not an allowable deduction.

Illustration:

Mr. A donated to Mr. B a parcel of land with a fair market value of P1,000,000.00 which is subject of a mortgage for P600,000.00.

If Mr. B assumes the mortgage, meaning he will pay the balance of the mortgage, then the net gift is P400,000.00.

This is because only P400,000.00 is the net economic benefit that accrued to Mr. B.

If Mr. B does not assume the mortgage, then the taxable net gift is the full P1,000,000.00.

Diminutions on the other hand are reductions on the donations given by the donor upon his specific instruction.

Illustration:

Mr. A donated P1,000,000.00 to Mr. B with a specific instruction that he will give to his brother Mr. C P300,000.00.

Thus, the net gift to Mr. B is only P700,000.00, the net economic benefit that accrues to him.

Computation of Tax

The computation of donor's tax is on a cumulative basis over a period of one calendar year.

This means for every donation, the previous donation/s made in the same calendar year are included in the computation of donor's tax liability of the donor.

Illustration:

Mr. A made the following donations:

February 1, 2018 - P2,000,000.00;

April 1, 2018 - P1,000,000.00; and

September 15, 2018 - P500,000.00.

The donor's tax liability is computed as follows:

February 1, 2018

Amount Donated: P2,000,000.00

Less: Exempt Gift: (-P250,000.00)

Net Gift: P1,750,000.00

Multiply: Donor's Tax Rate (6%): P105,000.00

Donor's Tax Due = P105,000.00

April 1, 2018

Amount Donated: P1,000,000.00

Add: February 1, 2018 donation: P2,000,000.00

Total Donation: P3,000,000.00

Less: Exempt Gift: (-P250,000.00)

Net Gift: P2,750,000.00

Multiply: Donor's Tax Rate (6%): P165,000.00

Total Donor's Tax Due: P165,000.00

Less: Donor's Tax Previously Paid: P105,000.00

Donor's Tax Still Due: P60,000.00

September 15, 2018

Amount Donated: P500,000.00

Add: February 1, 2018 donation: P2,000,000.00

Add: April 1, 2018 donation: P1,000,000.00

Total Donations: P3,500,000.00

Less: Exempt Gift: (-P250,000.00)

Net Gift: P3,250,000.00

Multiply: Donor's Tax Rate (6%): P195,000.00

Total Donor's Tax Due: P195,000.00

Less: Donor's Tax Previously Paid: P165,000.00

Donor's Tax Still Due: P30,000.00

Donations Between Husband and Wife

The husband and wife are considered as separate and distinct taxpayers for purposes of the donor's tax.

However, if what was donated is a conjugal or community property and only the husband signed the deed of donation, there is only one donor for donor's tax purposes, without prejudice to the right of the wife to question the validity of the donation without her consent pursuant to the pertinent provisions of the New Civil Code of the Philippines and the Family Code of the Philippines.

Illustration:

When Spouses A and B gifted their daughter C and her husband D, there are four (4) donations made, namely:

donations of A to C and A to D, and

donations of B to A and B to D.

Donation from Spouse A to Daughter C

Donation from Spouse A to Son-in-law D

Donation from Spouse B to Daughter C

Donation from Spouse B to Son-in-law D

Tax Credit for Donor’s Taxes Paid in a Foreign Country

Citizen and resident donors are taxable in all their donations of properties located within or without the Philippines.

✅ Thus, their donations abroad may also be taxable in the foreign country where their properties are located.

In order to avoid or at least minimize the effect of double taxation, a donor's tax credit on the donor's taxes paid in the foreign country is allowed in the Philippines.

Limitations on Tax Credit

The tax credit that may be allowed in the Philippines is subject to the following limitations:

The amount of the credit in respect to the tax paid to any country shall not exceed the same proportion of the tax against which such credit is taken, which the net gifts situated within such country taxable under this Title bears to his entire net gifts; and

The total amount of the credit shall not exceed the same proportion of the tax against which such credit is taken, which the donor's net gifts situated outside the Philippines taxable under this title bears to his entire net gifts.

In fine, the tax credit allowed shall depend on whether one foreign country or multiple foreign countries are involved.

One Foreign Country

The tax credit is whichever is lower of the actual donor's tax paid in the foreign country and the limit as determined below:

Limitation =

Net Taxable Gift-ForeignNet Taxable Gift-World Donor's Tax Due

Multiple Foreign Countries

Determine whichever is lower of the actual donor's tax paid in each of the foreign countries and the limit per country using the formula above.

Determine the total world donor's tax credit limit using the formula below:

Limitation =

Total Net Taxable Gift-ForeignNet Taxable Gift-World Donor's Tax Due

The allowable donor's tax credit is whichever is lower between the limitations in items 1 and 2 above.

Donor’s Tax Administration

Filing of Returns and Payment of Taxes

Any person making a donation, whether direct or indirect, is required to accomplish under oath a donor's tax return in duplicate.

A donor's tax return is filed for every donation.

The filing of return, however, is not required for donations specifically exempt under the Tax Code or other special laws.

The donor's tax return shall contain the following:

Each gift made during the calendar year which is to be included in computing net gifts;

The deductions claimed and allowable;

Any previous net gifts made during the same calendar year;

The name of the donee;

Relationship of the donor to the donee; and

Such further information as the Commissioner may require.

Considering that under the TRAIN Law, the six percent (6%) donor's tax rate applies regardless of who the donee is, Revenue Regulations No. 12-2018 removed the relationship of the donor to the donee as a required information in the return.

Time and Place of Filing of Donor's Tax Return and Payment of Donor's Tax

The donor's tax return must be filed within thirty (30) days after the date the gift is made or completed and the tax due thereon shall be paid at the same time that the return is filed following the pay-as-you-file system.

Unless the Commissioner otherwise permits, the return shall be filed and the tax paid to an:

authorized agent bank,

the Revenue District Officer,

Revenue Collection Officer, or

duly authorized Treasurer of the city or municipality where the donor was domiciled at the time of the transfer, or

if there be no legal residence in the Philippines, with the Office of the Commissioner.

In the case of gifts made by a non-resident, the return may be filed with the Philippine Embassy or Consulate in the country where he is domiciled at the time of the transfer, or directly with the Office of the Commissioner.

For this purpose, the term "Office of the Commissioner" shall refer to the Revenue District Office (RDO) having jurisdiction over the BIR-National Office Building which houses the Office of the Commissioner, or presently, to the Revenue District Office No. 39- South Quezon City.

Notice of Donation by a Donor Engaged in Business

In order to be exempt from donor's tax and to claim full deduction of the donation given to qualified donee institutions duly accredited by the Philippine Council for NGO Certification, Inc. (PCNC), the donor engaged in business shall give a notice of donation on every donation worth at least Fifty Thousand Pesos (P50,000.00) to the Revenue District Office (RDO) which has jurisdiction over his place of business within thirty (30) days after receipt of the qualified donee institution's duly issued Certificate of Donation, which shall be attached to the said Notice of Donation, stating that not more than thirty percent (30%) of the said donation/gifts for the taxable year shall be used by such accredited non-stock, non-profit corporation/ NGO institution (qualified-donee institution) for administration purposes pursuant to the provisions of Section 101(A)(3) and (B)(2) of the NIRC.